Pine Lawn, a small city in North Saint Louis County, has begun exploring the possibility of disbanding its police department. If the city did so, it would likely turn over policing duties to the Saint Louis County Police Department (which already handles policing for more than a dozen municipalities along with unincorporated areas) or the new North County Police Cooperative, formed by Wellston and Vinita Park.

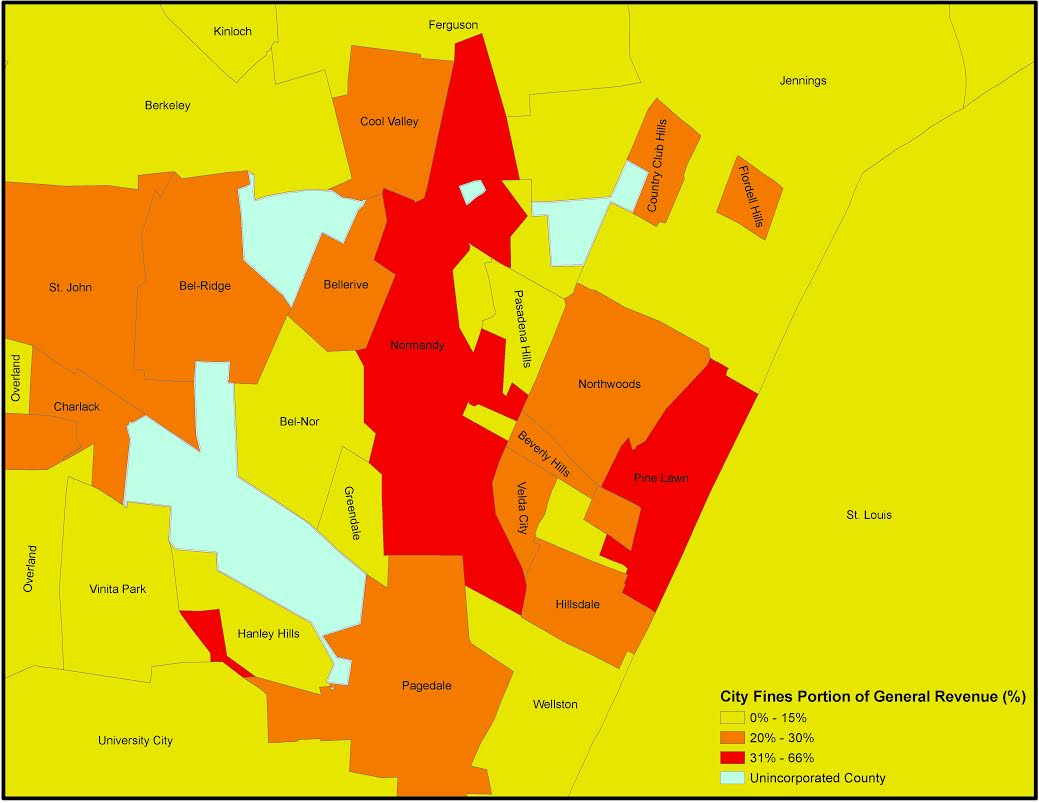

While the process through which the city is considering such a change has created considerable controversy, there is little doubt that Pine Lawn is in serious need of reform. The city been a posterchild of civic dysfunction, with a former mayor indicted for corruption, irregularities in city expenditures, and a highly criticized criminal justice system that uses poorly trained officers to fund the city through citations. Specifically addressing the last point, a report from Better Together showed that as of 2013 Pine Lawn relied on fines and fees for almost 50% of its general revenue, making it one of the worst offenders of the Macks Creek Law (which capped fines to 30% of general revenue) in Saint Louis County:

As we’ve written previously, until last this year the Macks Creek Law was regularly ignored and was without enforcement provisions. But with the passage of SB 5 in the last legislative session, things have changed. Cities like Pine Lawn can now collect no more than 12.5% of their general revenue via fines and fees. There are now regular reporting requirements, and failure to comply triggers a disincorporation vote.

These new legal provisions spell trouble for the status quo in Pine Lawn. Instead of a cash cow, their police force is likely to become a financial burden. That has pushed Pine Lawn and cities like it to do what they should have done a long time ago: join with the county or other cities to provide cost-effective and professional policing.