Everyone agrees that health care costs too much. The disagreements start when we have to decide who should receive less money. That’s a big reason why warnings about Medicaid “cuts” often receive so much attention. But the latest claims from Missouri hospitals about the One Big Beautiful Bill (OBBB) cuts hurting rural hospitals deserve a closer look.

At first glance, the concern seems straightforward. Since the government is the single largest purchaser of health care in the country, hospitals operating on thin margins could understandably struggle if they were paid less by Medicare or Medicaid. The first question, though, is what exactly is being cut.

The OBBB does not reduce the payment rates hospitals receive for treating Medicare patients or Medicaid patients who remain eligible. Instead, it implements community engagement requirements for some able-bodied Medicaid enrollees beginning next year, while changes to the provider tax financing system (explained more here) would not begin until 2028 at the earliest.

So, what are hospitals worried about? A recent KY3 report in Springfield provides some context. A spokesman for the Missouri Hospital Association explained that Medicare and Medicaid reimburse hospitals for only about 80 percent of the cost of providing care, describing the gap between costs and payments as “pretty enormous.” Mercy’s Sherry Clouse Day added that if someone loses Medicaid coverage under the new community engagement requirements, they may still seek care without insurance, leaving the hospital to absorb the cost.

That certainly could happen. But it assumes not only that a significant number of people will lose Medicaid coverage because of the new requirements, but also that many of them will become uninsured rather than finding work and obtaining employer-sponsored insurance or coverage through the Affordable Care Act marketplace.

That raises another question, though: If hospitals are already losing money treating Medicaid patients, why would treating fewer of them threaten their financial stability? Missouri hospitals already receive billions of taxpayer dollars every year through supplemental Medicaid payments and provider tax financing precisely because lawmakers recognize that Medicaid reimbursement often falls below the rates paid by commercial payers.

For those who have followed Missouri’s Medicaid debates for a while, this type of argument should sound familiar. Hospitals made similar claims during the campaign to expand Medicaid, arguing that adding more people to the program was necessary to protect rural hospitals. Today, even a policy change that doesn’t obviously reduce what hospitals are paid is being treated as a threat.

None of this is to say that lower Medicaid enrollment couldn’t result in less government money flowing to hospitals. But ultimately, hospitals are the only ones with a complete picture of how public dollars and other revenues from commercial payers affect their bottom line. After years of hospitals opposing efforts to bring greater transparency to their prices and financing, it’s fair to question yet another claim that a Medicaid policy change would threaten vulnerable hospitals. Before lawmakers accept those warnings, they should make sure there’s sufficient evidence to support the claim.

There are several cities and counties seeking to have new taxes or bond issues approved by voters on August 4. These include several major bond issues in Kansas City, a countywide use tax in St. Louis County, and sales or property tax increases in cities throughout Missouri, including in Hazelwood, Lee’s Summit, Ash Grove, and many more.

I’ll begin with the one local issue that is being voted on statewide (for various reasons that I won’t get into): Should the Jackson County assessor be an elected position? This is a pretty easy answer. Yes, it should be elected. Jackson County reassessments have been a disaster for over a decade now, and taxpayers have every right to be angry. Jackson County voters held the county executive responsible for it by recalling him, but being able to hold the assessor directly accountable is even better. St. Louis County changed its assessor from appointed to elected almost twenty years ago, and in my very informed opinion, the assessment process has improved since then. (Here are a few pieces on the general question on which positions should be elected and which should be appointed.)

St. Louis County has a countywide use tax on the ballot (again). A use tax is simply a sales tax imposed on goods you purchase online or through a catalogue and have delivered to your home. Municipal use taxes in Missouri actually predate the internet, but unsurprisingly most cities didn’t enact them until online shopping took off over the past fifteen years or so.

My view is that use taxes are a good way to expand the tax base, level the playing field for businesses, and raise local revenues. However, the last point is key. They should not be used simply as a way for cities to get more revenue, whether they need it or not. Cutting other taxes after the use tax is imposed—especially if you have a particularly harmful tax—is a great way to achieve the above benefits without a tax windfall for the county or city.

St. Louis County is having budget difficulties now, so I would understand primarily using the use tax money to address those issues. However, it would be even better if county leadership would agree to cut—at least in part—other taxes. I would suggest reducing the St. Louis County commercial property tax surcharge as a great place to start.

Kansas City is seeking approval for some substantial water and sewer bond issuances—about $750 million worth of each. There is nothing wrong with cities issuing bonds for infrastructure uses. It happens all the time, and there is a huge market for municipal bonds. If Kansas City is going to own and operate its water and sewer systems, it should invest in the system to prevent it from decaying, which is what happened to the water system in St. Louis. If that takes revenue bonds or price hikes, then so be it. (Note that these bonds will not, at least for now, require a tax increase.) So while I have no argument against approving these bond issues, I would also be remiss if I missed this opportunity to repeat that Kansas City would be even better off if it privatized its entire water and sewer system.

Remember, August 4 is a party primary election day, but you can always ask for a non-partisan ballot if you wish to vote on local ballot issues like these without voting in a party primary. The more you know . . .

On July 22, Missouri Attorney General Catherine Hanaway filed a lawsuit against Kansas City for violating anti-discrimination laws. A copy of the suit is available here.

For some background, I recommend you read my June 18 column for The Kansas City Star. In short, I detail a city council session in which the city’s own consultants report that after reviewing seven years of contracting data, they could find no evidence to support the need for the city’s race- and sex-conscious contracting preferences. In fact, the consultancy’s director of research told the council bluntly, “You just don’t have the factual predicate” required to continue such set-asides.

What that really means is that the city has no defense against a lawsuit.

Members of the council were not pleased with the report’s findings. They could have viewed this as a huge victory for Kansas City—having reached a point where such discriminatory programs were no longer necessary. Instead, council members chose to question the results and the methodology. Mayor Lucas even offered a novel legal theory: “The courts suck.”

We know that column, the only reporting I have been able to find about the consultants’ report, played a role in Hanaway’s suit because she tells us so. Not only does the lawsuit track with what I wrote, including Lucas’s petulance, but she explicitly cites the column in the suit’s footnotes.

Following up on my column, on June 26, I spoke with Lee’s Summit–based civil rights attorney Jonathan Whitehead on KCMO Talk Radio’s Mundo in the Morning. Whitehead details the legal history regarding race- and sex-based discrimination, the rules it put in place for allowing such programs, and how the findings in Kansas City may put the city in legal jeopardy.

As with the Star column, you won’t find any such in-depth interviews on the topic anywhere else.

Gov. Mike Kehoe recently signed House Bill (HB) 3231, a broad economic development package that revives the Missouri Downtown Economic Stimulus Act, better known as MODESA.

According to the Kansas City Business Journal, the revived program could help finance an expansion of CPKC Stadium, a possible new Royals ballpark, and billions of dollars in additional development connected to Kansas City’s Power & Light District and St. Louis’s Ballpark Village.

There are other provisions in the bill, including incentives for converting vacant office buildings into housing and programs tied to designated “innovation zones.” But the return of MODESA deserves particular attention because Missouri taxpayers already have some experience with the program. In Kansas City, that experience includes the Power & Light District.

Kansas City helped champion the original MODESA program in 2003, when downtown was struggling and city leaders were looking for ways to encourage investment. The program allowed new state tax revenues generated by qualifying developments to help finance projects, including public infrastructure associated with Power & Light.

The new version could be even more generous. The Business Journal reports that MODESA could redirect 50% of incremental state sales and employee income taxes generated by qualifying projects for as long as 30 years. For certain projects, that figure could rise to 70%. Local governments also would be required to provide substantial matching incentives.

Supporters believe the program can unlock investments that otherwise might not happen. The Cordish Companies, for example, says the legislation could help support $2.5 billion in new investment in Missouri, including an expansion that could “basically double” the size of the Power & Light District.

Perhaps. But before Missouri helps double the size of Power & Light, it is worth looking at how the financing of the original project has worked.

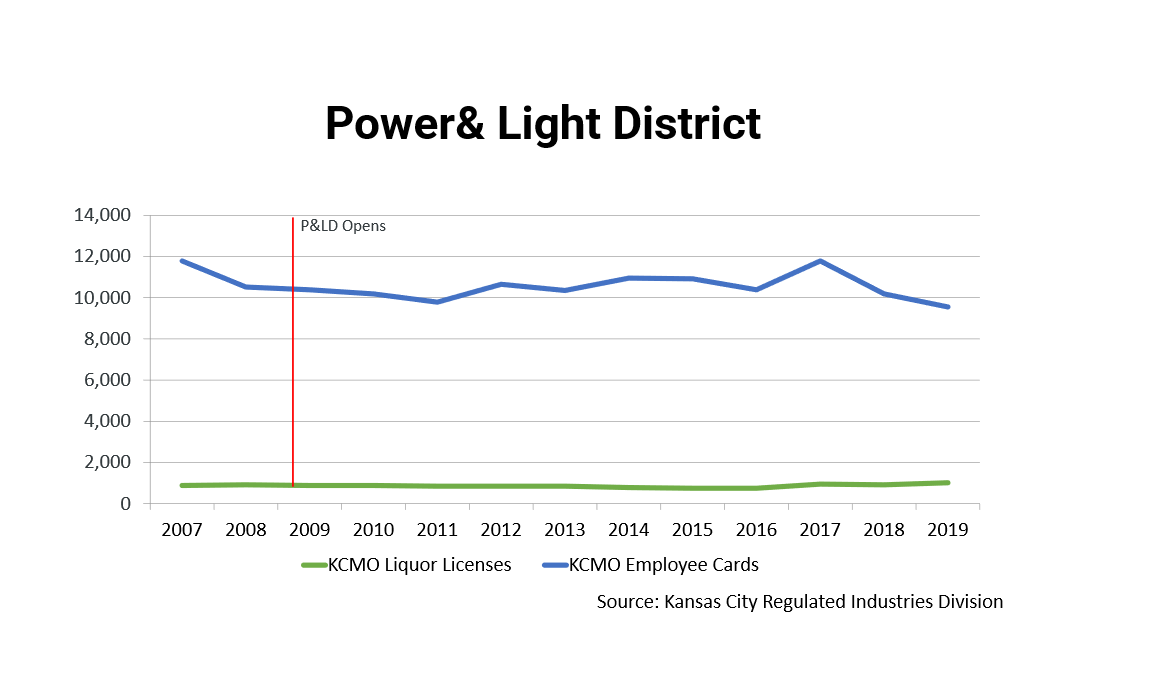

The district undoubtedly helped change the face of downtown Kansas City. It brought restaurants, bars, and entertainment venues to an area that badly needed investment. But it didn’t create new investment—it merely redirected economic activity at bars and restaurants from elsewhere in the city to downtown.

We know this because data provided by the city’s Regulated Industries Division shows us that the number of liquor licenses and employee cards required of bartenders and waitstaff remained flat after Power & Light opened. Despite new shops downtown, there was no growth citywide.

To make matters worse, the district has not generated enough revenue for Cordish to cover its debts. Because then-Mayor Kay Barnes was foolish enough to put taxpayers on the hook for debt payments, Kansas Citians have been paying out about $12 million each year over and above the tax revenue we divert back to the developer.

Kansas City is considering using the revived MODESA program as part of financing packages for an 18,000-seat expansion of CPKC Stadium and potentially a $3 billion Royals ballpark development at Crown Center. The city already has signaled its willingness to consider as much as $235 million in local incentives associated with the current project and $600 million for the Royals.

The state incentives are not insignificant, either. According to the Business Journal, the fiscal note for HB 3231 estimates the legislation will cost Missouri more than $62 million annually once fully implemented in 2034.

As Missouri leaders take on the task of cutting spending so that they may reduce and eventually eliminate the state income tax, these types of subsidies are not a sign of fiscal seriousness.

We’ve been here before. The effort failed. Why are we doubling down?

Missouri received a “B” on a national report card evaluating state policies on cell phone use in schools. This grade, available at phonefreeschoolsreport.org, places Missouri in the top half of states.

The primary reason for Missouri’s strong grade is its bell-to-bell ban on student cell phone use during the school day. State law also protects school employees from liability when they act in good faith to enforce the policy.

Missouri fell short of an “A” grade because students are allowed to store their phones in an accessible place during the school day. Only four states received “A” grades—Indiana, Kansas, North Dakota, and Rhode Island. They all require phones to be stored in an inaccessible location.

Overall, Missouri’s “B” grade is good news. Our lawmakers deserve credit for moving early on an issue where both common sense and research point in the same direction. Removing phone access during the school day is a straightforward solution to the obvious distractions that students’ devices bring into the classroom.

That said, our policy can be improved. When phones remain within arm’s reach—inside backpacks or pockets—there is temptation to use them. Requiring inaccessible storage would make enforcement easier and reduce classroom disruptions further. It would also align Missouri with the strongest policies in the country.

Missouri has taken an important step toward phone-free classrooms. Strengthening the law to require inaccessible storage would help get the most out of our students during school.

Susan Pendergrass speaks with Jude Schwalbach, senior policy analyst at Reason Foundation, about declining K-12 enrollment nationwide and what it means for the future of open enrollment. They discuss why enrollment dropped in 40 states since the pandemic, how districts have responded to increased competition from charter, private, and homeschooling options, why open enrollment tends to cause far less disruption than critics predict, the case for Missouri to catch up with its neighboring states, and more.

Susan Pendergrass (00:00):

Thank you so much. Jude Schwalbach, you’re back, I think for the third time, from the Reason Foundation. We appreciate you joining the Show-Me Institute Podcast once again, taking the time.

Jude Schwalbach (00:09):

Yeah, thank you for having me. I’m always excited to join.

Susan Pendergrass (00:26):

We were chatting for a second before we started recording. I talk about open enrollment a lot in Missouri. We don’t have it. In so many places in this country, kids choose where they go to school. They don’t just look at their utility bill, or their parents make this life-or-death real estate decision where they have to look at all the schools before they buy a house so they can pick where they go. Missouri has been really reluctant to let anybody choose a school over being assigned to one. I’ve been saying for some time that we have this phenomenon happening simultaneously: we don’t have as many kids anymore. I’ve talked to demographers on this podcast. We know that birth rates topped out in 2009, kindergarten enrollment topped out in 2013, and graduating high school seniors topped out a year or two ago. It’s a fact you can see all through the pipeline: there are fewer kids. In my mind, that’s going to make open enrollment more attractive, because we’re going to have districts that, for no explainable reason, just don’t have as many kids. Some of our top-performing districts, like Clayton, used to have 2,500 kids and now have 2,000. I keep thinking districts are going to wake up and realize they either have to fire teachers or get in the open enrollment game and actually have faith that they’ll attract students. You recently wrote about this, and that’s why I wanted to bring you on. Tell me what’s going on nationally with these enrollment trends and how you think that impacts this idea of whether kids should be assigned or allowed to pick.

Jude Schwalbach (01:51):

Yeah, so the latest national data we have on K-12 enrollments is from fall 2024. What we see is that in 40 states, K-12 enrollments dropped, by about 1.4 million students between 2019, right before the pandemic, and 2024. However, 10 states did manage to avoid those drops. In two of them, Florida and Utah, enrollments remained flat, they didn’t gain or lose students. The other eight states, places like North Dakota, Delaware, Alabama, and Texas, gained students. They really stand out because they gained students when literally everyone else lost students. They didn’t gain a ton, those eight states together gained around eighty thousand students, but when everyone else is losing and you’re gaining, you look pretty good. There are probably three factors driving this. As you mentioned, there are just fewer kids. The number of births in every single state except Florida

Susan Pendergrass (02:39):

Right.

Jude Schwalbach (02:53):

had dropped between 2014 and 2019, and those are the corresponding kindergarten cohorts five years later, 2019 to 2024. So there are just fewer kids. There’s also migration. There’s plenty of domestic migration occurring. In some states, especially the ones that gained students, they received quite a few new residents from other states. There’s also states, I think it was North Dakota actually, that lost a lot of residents through domestic migration but received a bunch of new residents from abroad, which reversed their general population decline and had them gain students. Presumably those families from abroad brought students with them, which is part of why they’re not losing students.

Susan Pendergrass (03:41):

Mm.

Jude Schwalbach (03:53):

There are various economic factors driving those things. But another component is that satisfaction with public schools is at an all-time low, especially post-pandemic.

Susan Pendergrass (03:50):

Yeah.

Jude Schwalbach (03:53):

Families are starting to choose schools other than public schools at a much higher rate than they used to, because they have more options. There are states with universal private school choice programs now, which ten years ago were just a pipe dream. You could achieve a small, targeted private school choice program, but not much more. Then there are families choosing homeschooling. This has created a much more competitive education marketplace. And it’s not just states with robust private school choice programs where you see increased private school enrollment. Places like California and New York, which have no private school choice, have also seen their private schools increase in popularity in the interim while public enrollment has been declining. So if you’re going to be in this tighter market with fewer students and increased competition from homeschools and private schools, you’re going to want to provide some flexibility within the public system to make it more attractive to families. Flexibility like open enrollment. Sorry, that was a really long answer.

Susan Pendergrass (04:59):

No, I think it’s perfect. It makes me think of the cliche of skating to where the puck is going, rather than where it is right now. I feel like a lot of the pushback from folks is they’re just looking at where the puck is right now. They’re like, well, we’ve got lower teacher-student ratios, fewer kids in every classroom, this is great. Or, bringing in a whole new topic here, the federal tax credit that’s looming for private school choice, where people can donate their tax dollars to a scholarship organization, and you have leadership in the teachers unions telling Democratic governors, you better not do this, because the way we’re going to keep the kids in the public schools is to lock them in. That seems so short-sighted to me, when, like you just said, we can look at the enrollment trends and know that while there are fewer kindergartners today, ten years from now there’s going to be another five to ten percent drop-off in kindergartners. Who are we kidding?

Jude Schwalbach (05:58):

Yeah. As that market gets tighter, the funding those students produce is going to become more important to public schools. If you look at California, there’s a report by their Legislative Analyst’s Office that found that districts initially losing students through open enrollment, where students were transferring to other districts with better test scores, or maybe they wanted different academic opportunities like AP classes, those districts reached out to families and said, what can we do to get you to stay? Families said, actually, we don’t want to leave the district, we just want to go to a different school inside our district. Or they said they wanted a language immersion class or something along those lines. The districts responded to families’ frustrations, and not only did some of them stop the bleeding, they actually gained students from other districts because they were doing something good that families wanted. So when you create a more flexible system, you shouldn’t just assume you’re going to lose students. There’s real opportunity to gain students as well.

Susan Pendergrass (07:09):

Yeah, I’ve certainly heard superintendents say it forced them to stop and think about what they offer. What is our mission? What do we offer? When you have a captive enrollment zone, you don’t need to do that. I studied this a long time ago in Massachusetts, and people would say, well, you can’t really prove that districts respond to competition. But I did research on it and talked to superintendents. They said, we moved the date of our orientation so kids would come visit our school first, or we redid parts of the school that parents had been complaining about. There are these little micro-responses, which is to say they realized that this is no longer a guaranteed monopoly. They have to start responding to families. And in the end, everyone kind of wins.

Jude Schwalbach (08:01):

Yeah, another good example that builds on what you were just saying is Minneapolis Public Schools. For the past ten years, their enrollments have been in decline, largely because of competition with charter schools and other public schools in the area. But recently they reversed that ten-year decline and gained new students, because when they were doing school tours, they started following up with parents, saying, we just want to remind you what you thought, and these are the options we offer that other districts nearby don’t.

Susan Pendergrass (08:24):

Yeah. What’d you think?

Jude Schwalbach (08:33):

This is what makes us a unique education option. I think it’s no surprise that families liked that personal touch and started enrolling in Minneapolis Public Schools.

Susan Pendergrass (08:40):

Yeah, we need it. I know you study school finance a lot too. I wonder, in Missouri anyway, certainly within St. Louis County but across Missouri generally, the number of teachers being hired has only continued to increase. There’s this belief that spending on public education should only go one direction, up, regardless of the number of students, and that the number of teachers should only go up. Our state education agency, one of their only five goals is more teacher certifications, more, more, more, as though there’s an ever-expanding pool of students without looking at the reality. Oddly, I just did a podcast on Social Security and they’re doing the same thing. They’re not looking at the reality of the number of workers, they’re just operating on the assumption that there will always be more. Our schools are doing bond referendums to build new schools in Columbia, Missouri, even though the new ones they just opened are under capacity. Their enrollment is down two or three percent and expected to go down more, but

Jude Schwalbach (09:50):

Yeah, I think state policymakers should take steps to encourage districts to be more thoughtful about how they’re using taxpayer dollars. Indiana, where I live, did something a couple of years ago where districts have to prepare for permanent closures if one of their school facilities has lost ten percent or more of its students over a five-year period. It’s basically saying, look, if you’re not able to attract new students, if your local enrollment is declining, we shouldn’t be keeping these facilities open and draining taxpayer dollars. To be fair, this is a really painful decision for communities. No one likes to close schools, no one likes to rearrange staff. But it’s not fair to taxpayers to keep funding and maintaining buildings that are really only educating a small fraction of students. Florida also publishes a report on school facility capacity, but most states don’t even make this information public. A good first step is just making this sort of data available so families and taxpayers, when they get approached about bonds or hear about decisions to hire more staff, can ask, if your enrollment is declining and your buildings are half empty, why are you doing this? This sort of information helps hold district administrators accountable.

Susan Pendergrass (11:13):

Yeah, and the way schools are funded, and have been for at least a hundred years, these are very long-term commitments, because school districts are in the real estate business. They buy the land, build the building, fund it over fifty years rather than leasing, like a lot of charter schools do. They’re in the business of buying land and building buildings. And teachers, that’s a twenty-five or thirty-year commitment too. That’s also hard to adjust down. There are ways to do it, but districts are making these long-term commitments without paying close attention to the trends happening right under their nose. It’s a very odd situation to me, because you can see this coming, and we’re not getting a response out of the system. And to your earlier point about school choice programs taking students, they’re taking the blame. They’re blaming school choice for the fact that they have to close schools when that’s not actually the reason.

Jude Schwalbach (12:15):

Yeah, there’s a really interesting paper, I think published by Thomas Dee from Stanford in the last couple of years, where he looked at why 1.8 million students left the public school system since the pandemic. He looked at increased competition from private school choice, homeschooling, and changing demographics, whether it’s families moving across state lines or lower birth rates. What he found is that he couldn’t explain why one-third of those students exited the public school system. It’s just unexplained. There are demographic factors, there’s increased competition, those certainly matter, but they aren’t the only reasons. We don’t even fully know why some of these students are exiting the public system. But you can’t change the fact that they are.

Susan Pendergrass (13:00):

And you don’t address it by locking the door. They want to close the gate and lock it to stop it, and that to me is the most short-sighted approach.

Jude Schwalbach (13:09):

Yeah, I think locking students within a particular system without allowing them any agency in school selection is really unfair. If states are going to require you to go to school, you should have some agency in what that school is, because education is a really personal experience.

Susan Pendergrass (13:27):

Mm-hmm.

Jude Schwalbach (13:28):

Maybe you don’t get along well with a particular teacher, or their teaching style isn’t a good fit for you, or maybe you’re being bullied at school. But where you go to school shouldn’t ultimately depend on your parents’ largest financial investment, which is very much constrained by their income. Increasing open enrollment options, where if there’s space available,

Susan Pendergrass (13:45):

Yeah, yeah.

Jude Schwalbach (13:50):

we’re not talking about building new facilities or hiring new teachers to accommodate these students, these are spots that are actually open right now, and allowing students who don’t live in that district or attendance zone to attend that school, I think that’s just a common-sense reform.

Susan Pendergrass (14:05):

Do you think declining enrollment is going to spur that into action more? Is it going to have an impact on whether states like Missouri consider open enrollment?

Jude Schwalbach (14:17):

It seems like it could go either way, honestly. If there’s declining enrollment, that means there are spots available and districts would have an incentive to try to attract new students from other places. But on the flip side, individuals don’t always see the opportunity, they only see the cost, which is, we could lose students. What’s interesting is that when you look at open enrollment programs across the nation, especially the largest ones with the most established data, places like Wisconsin, Colorado, or Florida, you don’t see massive enrollment fluctuations when these programs are launched or even soon afterward. Instead you see small, incremental change, which means districts have plenty of time to adjust. In some cases it could mean they actually reverse course and start gaining students. I know in Missouri there’s a lot of concern in rural areas that they’ll only lose students. But the irony is that if you look at Wisconsin, which also has a lot of school districts, around four hundred, their rural districts actually gained students on net in their most recent open enrollment report. Sure, they lost some students, but they ended up attracting more students from their suburban counterparts. I think rural districts can absolutely compete successfully

Susan Pendergrass (15:22):

Yeah, we have over five hundred.

Jude Schwalbach (15:44):

in a more competitive education marketplace.

Susan Pendergrass (15:47):

We actually just released a report saying exactly what you just said, by my colleague Dr. Cory Koedel, showing that there isn’t a massive, or really much of any, enrollment disruption in the first three or four years after these programs pass, in states that have had them for a long time or even a short time. There really isn’t a disruption in the way that, when a bill gets a committee hearing in Missouri, folks from the school boards association or superintendents association say, oh my god, we won’t be able to keep up, the kids will be coming and going, it’s going to completely throw off our enrollment. But we’ve found there really isn’t a massive disruption. On the one hand, you have a pretty low cost to districts. On the other hand, as you mentioned, there’s a really large benefit possible for an individual family who has a child they have to force onto the bus every day because they dread going to school due to their teacher, bullying, or whatever. It’s a big benefit at the individual level for those families, and the cost is really quite small or very dispersed.

Jude Schwalbach (16:49):

Yeah, one thing I’ll note is that it benefits districts as well. In California there are small rural districts that actively rely on K-12 open enrollment to keep their doors open. One administrator basically said, look, this doesn’t let us hire new staff, we’re not making money off this program, but we aren’t letting staff go either. We’re keeping our doors open and the lights on in our schools. If they didn’t have open enrollment, that would not be happening. They’d have to shut the school or let go of staff. It’s really important to remember this is a real opportunity for districts to gain students.

Susan Pendergrass (17:30):

Yeah. As Cory points out all the time, if you have a fourth grade classroom with ten students and you can add two or three more, your marginal cost is almost zero. You probably already have the textbooks, the computer, the desk is sitting there, it’s literally idle assets. And those three students, even if they don’t bring a lot of money with them depending on how the funding follows the student, that’s a very low marginal cost for some marginal revenue. I think the more districts see it that way, because I don’t think in Missouri that funding for education is going to continue to just go up. We have a tight budget and we know enrollment is going down. That’s going to be a whole new horizon for folks to accept. And partly, similar to the findings across those forty states, we have more old people. We have fewer young people, more old people, and older people are expensive and need a lot of services. So schools and assisted living facilities are going to be competing against each other in a sense, and I think the trend would suggest assisted living wins out because there’s more of those people and fewer children. Some of these trade-offs are going to have to be considered in a way that no one

Jude Schwalbach (18:44):

Yeah.

Susan Pendergrass (18:48):

seems to want to do. So is open enrollment growing across the country, stagnant, or on the decline?

Jude Schwalbach (18:49):

Yeah, I think that’s certainly correct. Since 2021, eighteen states have strengthened their open enrollment policy in some capacity.

Susan Pendergrass (19:06):

Okay. I know our neighbor Kansas did, right? Oklahoma too, our other neighbor.

Jude Schwalbach (19:10):

Yeah, Kansas did it, Oklahoma too. Several of your neighbors have improved their open enrollment policies.

Susan Pendergrass (19:17):

Well, Oklahoma has complete universal school choice. If you move across our northern border, you can pick public or private. If you move across our western border, you can pick any public school. The big pushback on that was that the highest-quality, most desirable districts would see a rapid influx, and they haven’t. In Oklahoma you can either pick a public school or take a tax credit for private school. Then we have Arkansas as a neighbor, and they’re also universal. We’re kind of getting surrounded by it and we’re just holding out as the last bastion

Jude Schwalbach (19:43):

Yeah.

Susan Pendergrass (19:51):

of assigned public schools.

Jude Schwalbach (19:52):

Yeah, I think Illinois and Kentucky are about on par with Missouri, but I think their programs are actually slightly better. Not by much, but

Susan Pendergrass (20:03):

We sort of write off Illinois, like, at least we’re not Illinois, but they have a lot of public sector problems. Yeah, we have no open enrollment, very limited charter schools, and a very small scholarship program. So ninety-five percent of our kids are going to their assigned public school with no other option besides virtual.

Jude Schwalbach (20:23):

Yeah. But to answer your question, I think there’s a real opportunity for open enrollment to continue to grow, especially in states, I think Nevada is a good harbinger of what could be coming. They passed a strong within-district open enrollment policy last year, and that was a bipartisan bill, championed by the governor and Senate leadership that was Democrat. I think part of the reason they wanted to do that was to strengthen their public school system, to ensure that students had a reason to invest in their public schools, especially low-income ones, and one of the ways they wanted to do that was through creating flexibility within the public system.

Susan Pendergrass (21:12):

Yeah.

Jude Schwalbach (21:12):

That was one of the compromises that occurred there. You also see that in Kansas. That was an earlier reform, but also a compromise. That one was passed by increasing funding for public schools, and Republicans got increased flexibility within the public school system for students.

Susan Pendergrass (21:18):

Yeah. I mean, when you poll parents it’s ridiculously popular. Everybody clearly wants to pick.

Jude Schwalbach (21:37):

Yeah, families really want these policies. I think residential assignment works for some people, that’s the form of school choice they like. They like being able to purchase a home in a district and be guaranteed a spot. But if there are extra seats, there should be students who can fill those seats, especially when funding is flexible and portable.

Susan Pendergrass (22:03):

I believe declining enrollment is going to motivate open enrollment. I have a very optimistic view of this: superintendents and school boards are going to wake up and say, our enrollment is declining, the only way we can turn this around is to try to get kids from across the lines. In St. Louis County we have more than a dozen school districts within one county, for reasons that would take a two-hour podcast to explain. It’s very easy for a child to just cross the street and be in a different district, and I feel like districts are going to have a wake-up call and start trying to get those kids from across the street rather than making their parents move. Because it’s going to be that or lay off teachers. You can only keep your teaching staff for a limited amount of time if your enrollment is going down and your schools are staying open.

Jude Schwalbach (22:58):

I think you’re right, Susan. When you look at the NCES projections, which are a little dated at this point, they anticipate losing millions more students by 2031.

Susan Pendergrass (23:08):

Yeah, yeah. So our heyday in Missouri, you could kind of say we had a million students, we had about 952,000 or so. If you wanted to round up, you’d say Missouri has about a million students. Now we have, depending on how you count pre-K and ungraded, somewhere between 830,000 and 850,000. And the NCES projections you just mentioned project that Missouri will be below 800,000, more like 785,000. We can’t even round up to a million anymore. We’re going to be more like 780,000. That’s more than a twenty percent loss, and that’s a lot.

Jude Schwalbach (23:58):

Yeah, enrollment declines aren’t new to the US. This happened in the seventies and eighties, but it took almost two decades for districts to recover their lost enrollment. That’s a long time, and it means you can’t hang on to buildings or staff in that interim when you don’t have the enrollment to justify them.

Susan Pendergrass (24:19):

Yeah, and I think in Missouri, good.

Jude Schwalbach (24:19):

I don’t think they returned to 1970 enrollment levels until 1997, if I remember correctly. There’s the baby bust,

Susan Pendergrass (24:31):

Wow, because the baby boom went through and then there’s a baby bust. But we don’t have a baby boomlet on the other side. There’s no evidence of one right now based on global trends.

Jude Schwalbach (24:39):

Yeah, it was fifteen years later before they even saw that sort of resurgence in births. They didn’t know either, and we don’t know either.

Susan Pendergrass (24:47):

Yeah. Yeah. I like that, that’s hopeful, that’s true. It just frustrates me, because if Missouri wants to hold out as the last residential-assignment state in the era of declining enrollment, I just feel like, there’s a professor from SLU, Ness Sandoval, who talks about Missouri demographics a lot, and he’s not optimistic about where we’re headed. One thing I think we could do to turn it around is throw open the doors on school choice to try to get families to locate here, but we’re kind of doing the opposite. Well, thanks so much. I appreciate you coming on and explaining it. I think it’s pretty interesting stuff, and I think we’re going to have to talk about this more as more enrollment numbers come in and we see how folks respond. I’m hopeful that Missouri legislators will get it and will press for it in the 2027 session. We’ll be pressing for it at the Show-Me Institute, but maybe I’ll use all of your data, Jude, and hope they read it and see what’s on the horizon. That would be awesome. Thank you so much, I appreciate it.

Jude Schwalbach (25:47):

That would be great. Thank you, Susan.

Imagine getting a large one-time bonus, then using that money to buy an expensive new car. There are some obvious parallels to Missouri’s budget.

Shortly before the June 30 deadline, Governor Kehoe signed Missouri’s more-than-$50-billion budget for fiscal year 2027, which began on July 1. He also issued about $53 million in vetoes and more than $400 million in spending restrictions. While the vetoes are generally in line with recent years, the expenditure restrictions are much larger than have been necessary in more than a decade. The restrictions also indicate that the governor believes the legislature approved roughly $400 million more in spending than projected state revenues can support.

Unlike a veto, a spending restriction doesn’t permanently eliminate an appropriation. Instead, it temporarily withholds the authority to spend it. Missouri’s constitution requires the governor to keep the budget balanced throughout the fiscal year, so if projected revenues won’t support all the spending approved by the legislature, the governor must reduce authorized spending through vetoes, restrictions, or a combination of both. The difference is that vetoes are permanent unless the legislature overrides them, while restrictions can be lifted if revenues improve. The governor then decides which restricted appropriations, if any, are ultimately released.

Perhaps the most interesting part of the governor’s budget signing was the explanation he provided for this year’s actions. Kehoe reiterated something he’s said before: Missouri has a spending problem rather than a revenue problem. He also said the state needs to reduce its reliance on what are called general revenue pickups. General revenue is the state’s primary operating fund, supported largely by income and sales taxes. A general revenue pickup occurs when a temporary funding source disappears, leaving general revenue to cover an ongoing expense. That’s exactly how temporary spending becomes a permanent obligation.

The governor’s explanation reflects two concerns I’ve written about repeatedly. First, Missouri’s spending has been growing faster than its revenues. As the auditor has highlighted, between fiscal years 2020 and 2025, general revenue collections increased 45.8 percent. During that same period, general revenue spending increased 53.4 percent, more than double the rate of inflation.

Second, lawmakers treated the surge in temporary federal COVID relief and an extraordinary period of state revenue growth as an opportunity to expand ongoing commitments. As those temporary dollars disappeared, the state became increasingly reliant on general revenue pickups, shifting costs that had once been covered by other funding sources onto Missouri taxpayers.

Remember the car? If soon after your purchase you found you couldn’t afford your new car, nobody would say you had an income problem. They’d rightfully say you spent too much. Missouri’s budget shouldn’t be viewed differently. The good news is that Governor Kehoe’s actions indicate he has correctly identified the problem. Now it’s up to lawmakers to get serious about solving it.

Most schools embraced digital learning during and after the COVID pandemic, dramatically increasing students’ screen time during the school day. Combined with the long hours many children already spend on screens outside of school, the result has been an unprecedented amount of daily screen exposure.

But people are starting to push back. More than half of states have policies that limit or fully ban cell phones in schools. And many states and school districts have also enacted, or are considering, policies that limit screen use for instruction. Patrick Johann recently reviewed an instructional-use screen time policy adopted by the Los Angeles Unified School District, which is scheduled to take effect this upcoming school year.

Missouri is part of this broader trend. Last year the state banned cell phone use during the school day, and lawmakers debated the Student Screen-Time Standards Act during the 2026 legislative session, which would have curbed screen use for instruction. The Student Screen-Time Standards Act didn’t pass into law, but similar legislation will almost surely be introduced in 2027.

The rationale for cell-phone bans is that cell phones are a distraction. For laws that limit screens for instructional use, the idea is that screen-based instruction simply does not produce as much learning as face-to-face teaching. Technology offers many benefits, but it has been unable to replace the human interaction that many students—especially those from disadvantaged backgrounds—need to thrive in school.

If we had a robust market for school choice, I would welcome schools that make technology central to their instructional model. Some students will undoubtedly flourish in those environments, and technology can support a level of personalized instruction that is difficult to achieve in a traditional classroom. Alpha School is an interesting model with promising early results.

But in states like Missouri, where most students are still required to attend their residentially zoned public school, school districts should not use learning models that don’t benefit most students.

A recent article at The74 discusses an unlikely ally in all of this: students themselves. The article explains how many students describe their relationship with technology in terms that resemble addiction. The author writes:

They don’t want to be on their phones eight or nine hours a day. They don’t want to use AI to complete their assignments and short-circuit their ability to learn and grow. They know their attention span is stunted. But in so many circumstances, they simply can’t resist.

When the pandemic hit, schools shifted quickly toward technology-based instruction. It all happened very fast. However, as is often the case in such circumstances, the pendulum may have swung too far. Perhaps the clearest sign is the growing consensus for a course correction—from parents to teachers to policymakers and, increasingly, to students themselves.

The federal government will roll out a new tax-credit program in 2027 to expand school choice. Taxpayers will be able to receive a dollar-for-dollar federal tax credit for donations of up to $1,700 annually to a scholarship-granting organization (SGO) in Missouri—or any other participating state. The SGO then distributes scholarships to families seeking alternatives to their residentially assigned public schools.

In a previous post I wrote about the new program, focusing on the challenge of deciding which educational expenses should qualify for scholarship funding.

Over at Education Next, Rick Hess has a thoughtful piece on other aspects of the program. As both a school choice advocate and an advocate of fiscal responsibility, he opens with a concession, acknowledging the potential loss of tax revenue the program could create at a time when the federal debt is growing rapidly.

He then makes what I think is the right point: While it is unfortunate that the federal budget is off the rails, it is hard to get too worked up about this program when (a) it is a drop in the bucket compared to our broader fiscal problems, and (b) so much of our debt-financed spending benefits older Americans. If we’re going to keep borrowing, why not direct at least a small share toward expanding opportunities for children?

I share Hess’s bottom-line sentiment. I wish the federal government managed its finances more responsibly. But since that does not appear likely anytime soon, investing a bit more in the children who will ultimately inherit—and help repay—that debt seems sensible to me.

Turning to the program itself, Hess raises an important practical concern. Even though this is a dollar-for-dollar tax credit, which means it is effectively costless for taxpayers to participate, we should not assume it will be widely used. Many taxpayers may be unaware the credit exists. Others may doubt they’ll actually receive it or may not know how to make a qualifying donation to an SGO. Even modest uncertainty or inconvenience can discourage participation.

These are legitimate concerns. The new scholarship tax credit has the potential to generate substantial resources to expand school choice, but realizing that potential is not automatic. As Hess puts it, “I don’t put a lot of stock in the casual assurance that taxpayers will jump through hoops to give money away simply because, as one very prominent champion explained to me, ‘It’s a good thing to do.’”

Hess’s piece points to one of the program’s biggest implementation challenges. Helping taxpayers understand the credit—and making participation as simple as possible—could make an enormous difference. Show-Me Institute analysts will certainly be doing our part, and I hope many others will as well.

Support Us

The work of the Show-Me Institute would not be possible without the generous support of people who are inspired by the vision of liberty and free enterprise. We hope you will join our efforts and become a Show-Me Institute sponsor.