Kansas City Teacher Pension Faces Possibility of Insolvency

In 20 years, the probability that the Kansas City Public School Retirement System (KCPSRS) will not be insolvent is only somewhat better than a coin flip. Don’t take my word for it—just take a look at the report from Segal Marco Advisors which was commissioned by the board of KCPSRS. The report, which was presented to the board but not widely distributed, paints a bleak picture for the defined-benefit pension system. It illustrates what Show-Me Institute analysts have been saying for years: these systems face many obstacles and should be more transparent.

When Michael Rathbone and I released our report, “Betting on the Big Returns: How Missouri Teacher Pension Plans Have Shifted to Riskier Assets,” in 2015, we stated that pension plans should be more transparent about funding possibilities. We wrote:

To improve transparency, lawmakers could require pension plans to forecast assets using multiple assumptions on investment returns. What would the funding ratio for each of these plans be if returns are 4 percent or 6 percent instead of 8 percent? This is something policymakers should know as it would allow them to choose the best way to structure contributions so that downside is minimized and that these plans can be adjusted to adapt to any unexpected downturns that may occur.

The report is exactly what we called for. It illustrates how the forecasts of the health of the system will be affected by varying contribution rates and investment return assumptions. Here and in a follow-up post I will present some of the findings from the KCPSRS report.

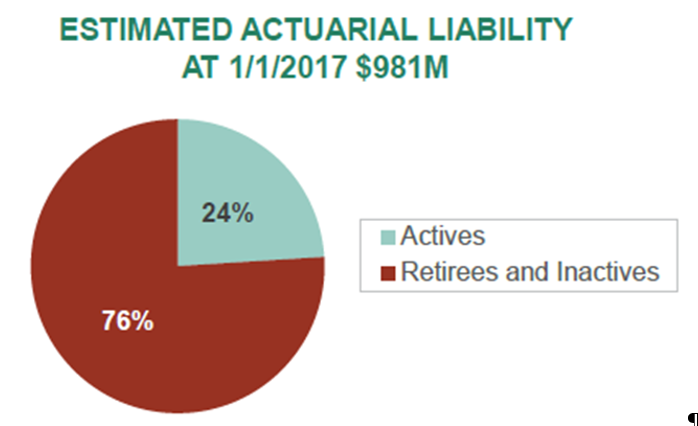

The main takeaway is that the system could be in serious trouble within the next two decades. Currently, the system is 64% funded with $349 million in unfunded liabilities. Next year, the plan expects to pay out $85 million in benefit payments. In contrast, the system will only collect $33 million in pension contributions. This is because the participants in the plan are trending older and older. Today, more than three-fourths of the members of KCPSRS are retirees:

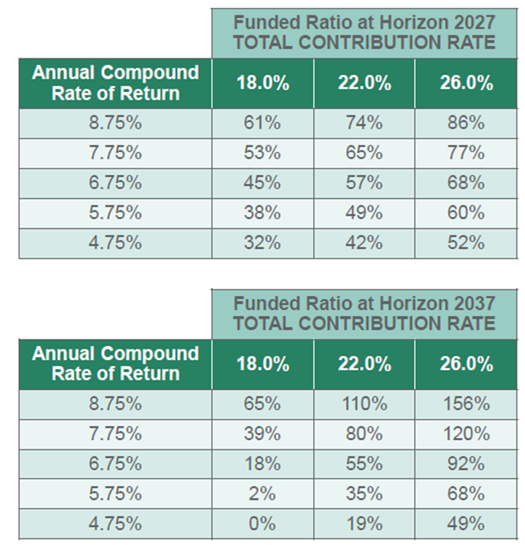

The tables below present projections for the funded ratio over 10 and 20 years under different scenarios that take into account various rates of return and contribution rates. Currently, active members of KSPSRS and their employers each pay 9 percent of salary into the system for a contribution rate of 18 percent.

The best-case scenario within 10 years is that the system will improve to an 86% funded ratio. If the plan doesn’t make any changes to contribution rates and receives the expected rate of return of 7.75 percent (the actuarially assumed rate), the funded ratio will drop to 53%. In 20 years, the funded ratio could continue to drop to less than 40 percent.

But here’s the real kicker, the authors write that “The probability of insolvency is 2% at the 10 year horizon and increases substantially to 42% at the twenty year horizon.” You read that right. Within 20 years there is a real possibility that the KCPSRS could be insolvent. We hear all the time that these defined-benefit plans are great for retirees. Well, not if they are bankrupt.

In my next post, I’ll discuss how the system may address the issue of unfunded liabilities.