What’s $65 Billion between Friends?

We teach kids the value of properly saving when they’re young, but when it comes to public pensions, retirement funds might not be quite what we once thought. In June the Mercatus Center published the 2016 edition of its annual “Ranking the States by Fiscal Condition” report. Missouri ranked 14th overall, but the red flag from this report regards nationwide pension plan funding (or lack thereof).

For those unfamiliar with the current pension debate, here’s a crash course: A pension plan’s funding ratio is the value of its assets (contributions to date) divided by the present value of its liabilities (discounted sum of its future payments). Between today and when the future payments are due, contributions will be put in and investment returns will be realized on the plan’s assets. Of course, the future contributions necessary to ensure a fully funded plan depend on the returns that are realized. In other words, if a plan’s returns fall short then contributions will have to fill in the gap. Current General Accounting Standards Board practices allow a pension fund to discount its future payments at the rate that fund managers expect returns to achieve, but in recent years economists have argued against valuing a plan’s funding ratio this way due to the simple fact that while investments might reach the expected goal, the funds for retiring employees must be paid.

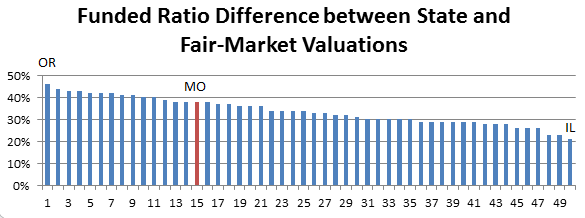

Many economists note that current estimations don’t guarantee goals will be met, and that the safer way to estimate how well-funded a plan is involves discounting future payments as if they came from risk-free investments (i.e., treasury bonds). Mercatus listed each state’s funding status, first according to the state’s assumed investment return rate and then according to the risk-free rate, revealing a staggering gap. The graph below shows the difference between the ratios using the assumed rate and the risk-free rate for each state.

When determining a state’s funding ratio, the two methods produce an average difference of 34%. Missouri’s funding ratio drops 38%, with a difference of 64.84 billion (yes, that’s billion with a B). To be clear, this chart does not mean taxpayers will have to make up all or part of the difference, but the discrepancy in valuation shows the drastic potential costs taxpayers could be burdened with if investment returns don’t live up to their current expectations.

The types of investments that pension plans hold are up to the discretion of their managers, but these numbers are no small chunk of change. If states are going to guarantee retirement funds, they may want to consider a risk free measurement system that will ensure they are prepared to pay employees what is promised.